Usually, starting an article with a definition is not being thought on writing masterclasses. However, for the sake of readers with little background knowledge about digital wealth management, here’s what Investopedia says about the topic I am about to cover.

“Robo-advisors are digital platforms that provide automated, algorithm-driven financial planning services with little to no human supervision.”

In other words, I will try to depict why the computerized equivalent of human investment managers is getting more and more attractive for those who seek to invest their savings.

Trends in the wealth management industry

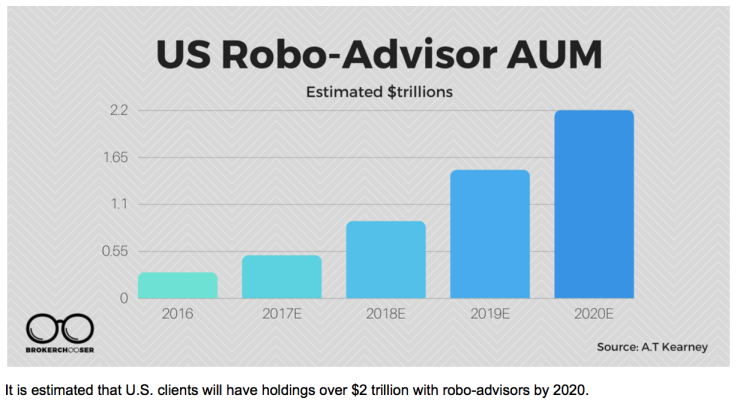

The Big Bang of digital investing happened in 2008 when a company called Betterment – since being top US robo-advisor – emerged on the horizon. According to Statista, it is estimated that by 2021 there will be more than 11 million US clients using robo-advisory services.

So what is happening with the incumbent firms then? Can we say farewell to traditional funds and human financial advice? Not really.

Reading through this year’s Global Asset Management report prepared by the experts of Boston Consulting Group, it is clear that the AUM (assets under management) growth is slowing and pretax profit margins are melting for traditional asset managers.

In spite of fierce price competition and tougher regulation, managing funds is still a profitable venture. The question arises, how much profit is generated by disruptive robo-advisors? Mainly none. The oldest player, Betterment with an $800 million valuation is in the red yet, and so are the others. The reason why not being profitable is not a real disadvantage for robo-advisors is that both major stakeholders – venture capitalists and customers – trust in these firms. And they do it for the right reason.

Performance and fees

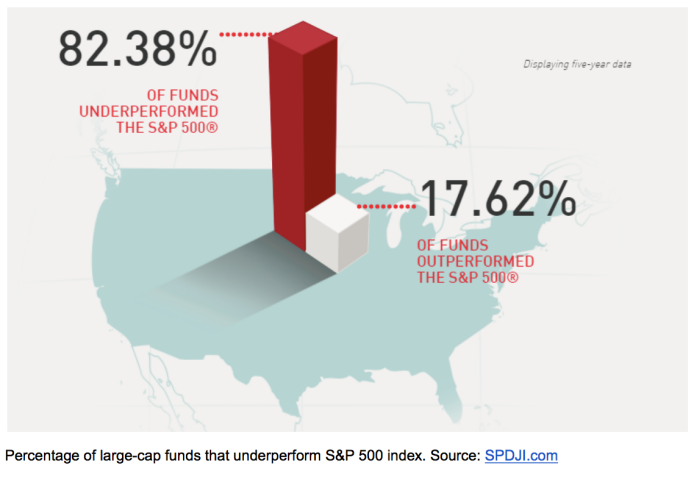

It is a widely known fact that since the outburst of the financial crisis, active fund managers struggle to beat their own benchmarks. Due to this continuous underperformance and exorbitant fund fees, allowing fund managers to live the Wolf of Wall Street lifestyle, the attractiveness of such funds failed. Passive investing, buy and hold strategies came to the forefront, with very strong tailwinds from investment gurus like Warren Buffet.

The wave of discontent that posed challenge for traditional funds led to the rise of ETF based automated portfolio investments. Exchange traded funds are available to all retail investors, they are really cheap (in some cases can be even commission free) and they include diversification by their nature.

From this point, digital advisors had two tasks to accomplish additionally. One is customer profiling and the other is portfolio rebalancing. First is a process of mapping out the risk tolerance and investment goals of individuals, and the second is a technical step that keeps the right asset allocation on track while the market is moving. Both were a child’s play for programmers.

Digital platforms, mobile breakthrough

Beside the great value for price combination of automated financial service providers there is a user experience factor to success. Visiting the website of robo-advisors is a real visual joy. Since these companies come from startup backgrounds they all have learned how to focus on their customer’s needs.

The apps and digital platforms they present state clearly what are the holdings of the portfolio and show graphs of the net returns in real time. Deposits and withdrawals can be easily made and reviewing investment goals is also a basic option.

No wonder Millennials are crazy for robos and most likely they will never visit the skyscrapers of Wall Street to chat with human private bankers.

Finally, there are some really surprising recent app developments like the ability to trade on Facebook Messenger. This is a feature available for TD Ameritrade customers who initially received market news and education through an AI fueled chatbot. This bot has been further developed in order to enable trading equity and ETF instruments.

Future direction of digital investing

Looking at the current trends it is very likely that young and first-time investors will start their journeys by default at digital financial service providers, and most likely the incumbent firms will further incorporate disruptive technologies through partnerships, mergers, and strategic buyouts.

There is a huge question mark around artificial intelligence and how it might enhance investment decision making. Just to name few options, investor sentiment analysis, pattern-based future price prediction, machine learning fueled chatbot advisory all are possible features becoming mainstream in the near future.